![]()

Time Series Analysis

introml.analyticsdojo.com

59. Time Series Analysis#

import numpy as np

import pandas as pd

import os

import yfinance as yf

import matplotlib.pyplot as plt

import seaborn as sns

from statsmodels.tsa.seasonal import seasonal_decompose

#!pip install yfinance

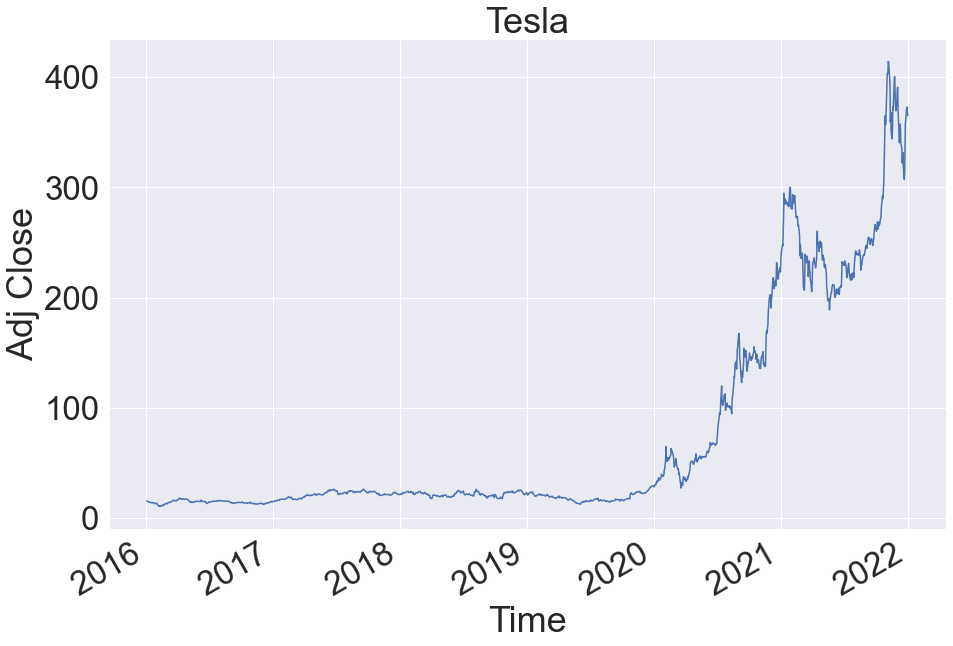

data = yf.download(tickers="TSLA", start="2016-1-1",end="2021-12-31",progress=False)

data.head()

| Open | High | Low | Close | Adj Close | Volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2016-01-04 | 15.381333 | 15.425333 | 14.600000 | 14.894000 | 14.894000 | 102406500 |

| 2016-01-05 | 15.090667 | 15.126000 | 14.666667 | 14.895333 | 14.895333 | 47802000 |

| 2016-01-06 | 14.666667 | 14.670000 | 14.398667 | 14.602667 | 14.602667 | 56686500 |

| 2016-01-07 | 14.279333 | 14.562667 | 14.244667 | 14.376667 | 14.376667 | 53314500 |

| 2016-01-08 | 14.524000 | 14.696000 | 14.051333 | 14.066667 | 14.066667 | 54421500 |

plt.rcParams["figure.figsize"] = (15,10)

sns.set(font_scale=3)

data['High'].plot()

plt.xlabel('Time')

plt.ylabel('Adj Close')

plt.title('Tesla')

Text(0.5, 1.0, 'Tesla')

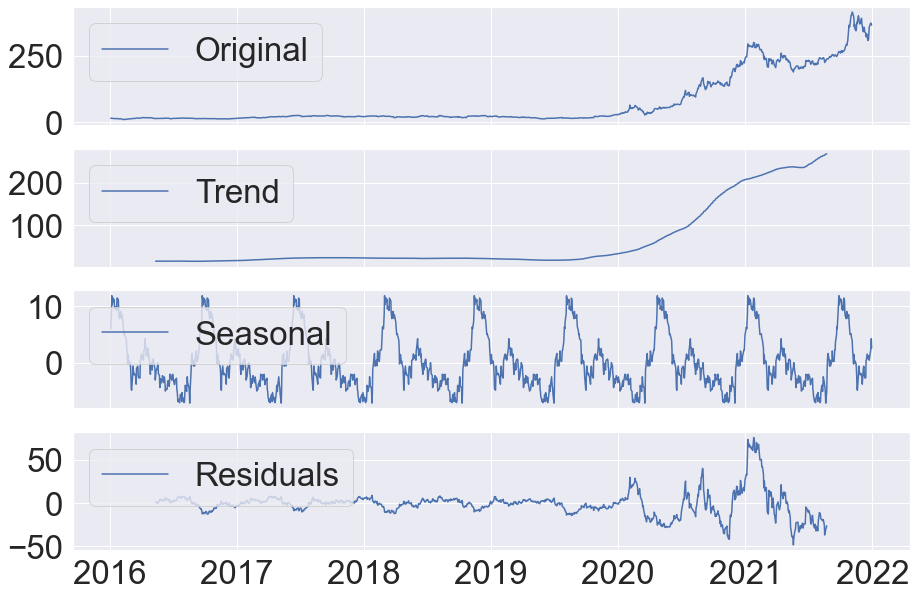

#Select frequency based on no of observations that comprise a cycle in the dataset

ts_decompose_add = seasonal_decompose(x=data['High'],

model='additive',

freq=180)

estimated_trend_add = ts_decompose_add.trend

estimated_seasonal_add = ts_decompose_add.seasonal

estimated_residual_add = ts_decompose_add.resid

<ipython-input-15-ada5a077c2aa>:2: FutureWarning: the 'freq'' keyword is deprecated, use 'period' instead

ts_decompose_add = seasonal_decompose(x=data['High'],

fig, axes = plt.subplots(4, 1, sharex=True, sharey=False)

# fig.set_figheight(10)

# fig.set_figwidth(15)

axes[0].plot(data['High'], label='Original')

axes[0].legend(loc='upper left');

axes[1].plot(estimated_trend_add, label='Trend')

axes[1].legend(loc='upper left');

axes[2].plot(estimated_seasonal_add, label='Seasonal')

axes[2].legend(loc='upper left');

axes[3].plot(estimated_residual_add, label='Residuals')

axes[3].legend(loc='upper left');