![]()

MA, AR, and Arma

introml.analyticsdojo.com

60. MA, AR, and Arma#

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from matplotlib.pylab import rcParams

rcParams['figure.figsize'] = 15, 5

import seaborn as sns

!pip -q install yfinance

import yfinance as yf

####Moving Average analysis

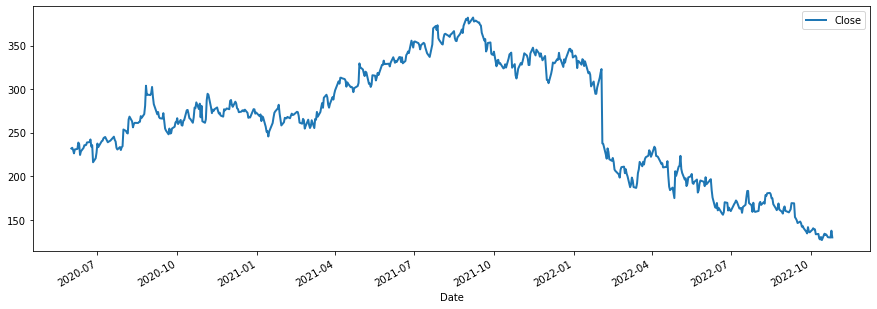

FB = yf.Ticker("META")

# get historical market data

FB_values = FB.history(start="2020-06-01")

FB_values[['Close']].plot(lw=2)

<AxesSubplot:xlabel='Date'>

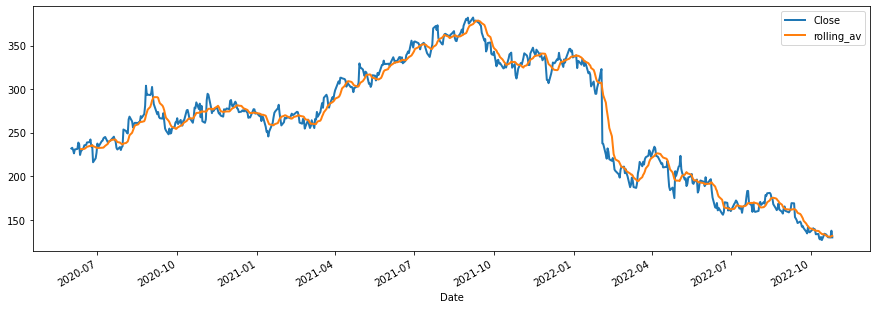

#Rolling average

FB_values['rolling_av'] = FB_values['Close'].rolling(10).mean()

# take a look

FB_values[['Close','rolling_av']].plot(lw=2)

<AxesSubplot:xlabel='Date'>

from statsmodels.tsa.arima.model import ARIMA

ARMA_model = ARIMA(endog=FB_values['Close'], order=(0, 0, 10))

results = ARMA_model.fit()

print(results.summary())

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/statespace/sarimax.py:978: UserWarning: Non-invertible starting MA parameters found. Using zeros as starting parameters.

warn('Non-invertible starting MA parameters found.'

SARIMAX Results

==============================================================================

Dep. Variable: Close No. Observations: 608

Model: ARIMA(0, 0, 10) Log Likelihood -2709.211

Date: Wed, 26 Oct 2022 AIC 5442.423

Time: 19:26:34 BIC 5495.345

Sample: 0 HQIC 5463.012

- 608

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 263.6635 7.284 36.199 0.000 249.388 277.939

ma.L1 0.7786 0.019 40.264 0.000 0.741 0.817

ma.L2 0.3297 0.013 24.505 0.000 0.303 0.356

ma.L3 0.1467 0.011 12.936 0.000 0.125 0.169

ma.L4 0.9416 0.011 87.808 0.000 0.921 0.963

ma.L5 1.0996 0.019 59.397 0.000 1.063 1.136

ma.L6 0.8785 0.020 44.231 0.000 0.840 0.917

ma.L7 0.1297 0.013 10.040 0.000 0.104 0.155

ma.L8 0.3853 0.013 29.529 0.000 0.360 0.411

ma.L9 0.8021 0.015 53.684 0.000 0.773 0.831

ma.L10 0.8761 0.019 46.821 0.000 0.839 0.913

sigma2 439.7564 29.343 14.987 0.000 382.245 497.268

===================================================================================

Ljung-Box (L1) (Q): 224.32 Jarque-Bera (JB): 19.29

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 6.97 Skew: -0.39

Prob(H) (two-sided): 0.00 Kurtosis: 3.40

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/base/model.py:566: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

warnings.warn("Maximum Likelihood optimization failed to "

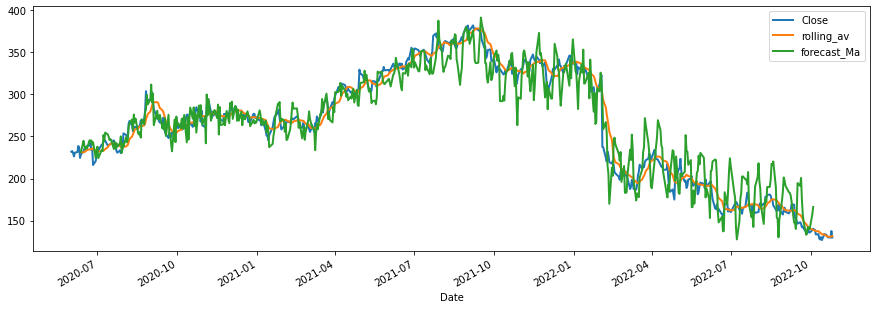

start_date = '2020-06-12'

end_date = '2022-10-04'

FB_values['forecast_Ma'] = results.predict(start=start_date, end=end_date)

FB_values[['Close','rolling_av','forecast_Ma']].plot(lw=2)

<AxesSubplot:xlabel='Date'>

# A Mojaor flaw is that the time series may not be stationary. It has to be done on returns

####Auto Regressive analysis

ARMA_model = ARIMA(endog=FB_values['Close'], order=(10, 0,0))

results = ARMA_model.fit()

print(results.summary())

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

SARIMAX Results

==============================================================================

Dep. Variable: Close No. Observations: 608

Model: ARIMA(10, 0, 0) Log Likelihood -2051.121

Date: Wed, 26 Oct 2022 AIC 4126.243

Time: 19:26:35 BIC 4179.165

Sample: 0 HQIC 4146.832

- 608

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 263.6740 509.998 0.517 0.605 -735.904 1263.252

ar.L1 0.9530 0.050 18.994 0.000 0.855 1.051

ar.L2 0.0623 0.062 1.004 0.315 -0.059 0.184

ar.L3 -0.1102 0.053 -2.090 0.037 -0.214 -0.007

ar.L4 0.0396 0.051 0.768 0.442 -0.061 0.140

ar.L5 0.0193 0.054 0.355 0.722 -0.087 0.126

ar.L6 0.0225 0.056 0.399 0.690 -0.088 0.133

ar.L7 -0.0239 0.057 -0.422 0.673 -0.135 0.087

ar.L8 0.0016 0.070 0.022 0.982 -0.136 0.139

ar.L9 0.0922 0.076 1.211 0.226 -0.057 0.242

ar.L10 -0.0570 0.053 -1.072 0.284 -0.161 0.047

sigma2 49.3269 1.286 38.352 0.000 46.806 51.848

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 26048.16

Prob(Q): 0.96 Prob(JB): 0.00

Heteroskedasticity (H): 2.02 Skew: -2.53

Prob(H) (two-sided): 0.00 Kurtosis: 34.66

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

start_date = '2020-06-12'

end_date = '2022-10-04'

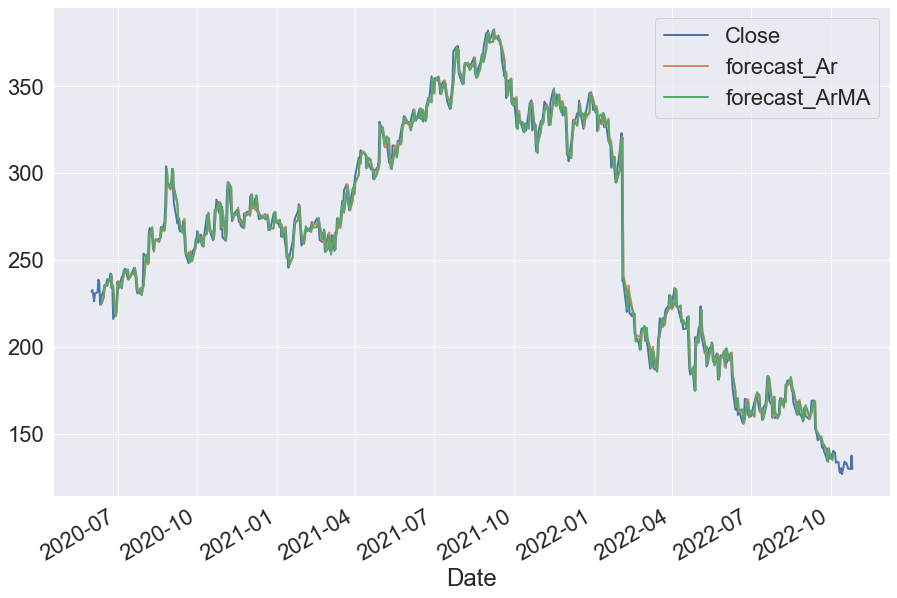

FB_values['forecast_Ar'] = results.predict(start=start_date, end=end_date)

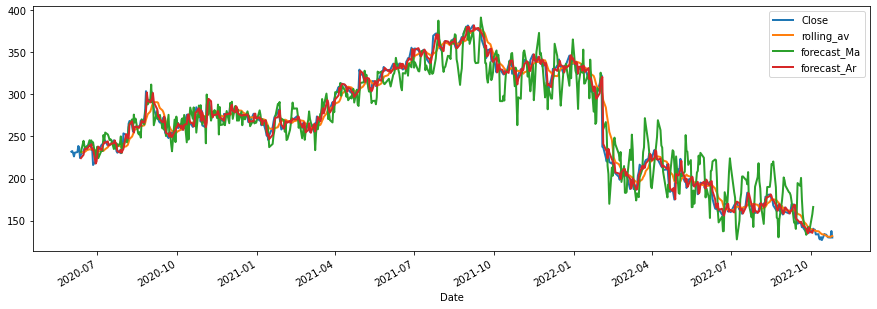

FB_values[['Close','rolling_av','forecast_Ma','forecast_Ar']].plot(lw=2)

<AxesSubplot:xlabel='Date'>

####Now lets do AR & MA

ARMA_model = ARIMA(endog=FB_values['Close'], order=(10, 0,10))

results = ARMA_model.fit()

print(results.summary())

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/statespace/sarimax.py:966: UserWarning: Non-stationary starting autoregressive parameters found. Using zeros as starting parameters.

warn('Non-stationary starting autoregressive parameters'

SARIMAX Results

==============================================================================

Dep. Variable: Close No. Observations: 608

Model: ARIMA(10, 0, 10) Log Likelihood -2048.853

Date: Wed, 26 Oct 2022 AIC 4141.706

Time: 19:26:37 BIC 4238.730

Sample: 0 HQIC 4179.453

- 608

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 263.6608 77.496 3.402 0.001 111.771 415.551

ar.L1 0.3242 10.387 0.031 0.975 -20.035 20.683

ar.L2 0.6924 8.735 0.079 0.937 -16.428 17.813

ar.L3 -0.0474 2.440 -0.019 0.985 -4.830 4.735

ar.L4 -0.4487 1.723 -0.260 0.795 -3.826 2.929

ar.L5 0.0365 3.563 0.010 0.992 -6.946 7.019

ar.L6 0.3317 2.301 0.144 0.885 -4.179 4.842

ar.L7 -0.1589 2.141 -0.074 0.941 -4.355 4.037

ar.L8 -0.4674 2.951 -0.158 0.874 -6.252 5.317

ar.L9 0.4247 3.224 0.132 0.895 -5.893 6.743

ar.L10 0.2979 6.117 0.049 0.961 -11.692 12.288

ma.L1 0.6286 10.385 0.061 0.952 -19.726 20.984

ma.L2 -0.0274 1.333 -0.021 0.984 -2.639 2.585

ma.L3 -0.0354 0.766 -0.046 0.963 -1.537 1.466

ma.L4 0.3989 0.523 0.762 0.446 -0.627 1.424

ma.L5 0.4050 3.963 0.102 0.919 -7.362 8.172

ma.L6 0.1198 2.022 0.059 0.953 -3.844 4.083

ma.L7 0.2405 0.631 0.381 0.703 -0.997 1.478

ma.L8 0.6664 2.667 0.250 0.803 -4.561 5.893

ma.L9 0.3085 5.696 0.054 0.957 -10.855 11.472

ma.L10 0.0216 0.318 0.068 0.946 -0.601 0.645

sigma2 49.3105 1.759 28.029 0.000 45.862 52.759

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 25080.34

Prob(Q): 0.97 Prob(JB): 0.00

Heteroskedasticity (H): 1.99 Skew: -2.45

Prob(H) (two-sided): 0.00 Kurtosis: 34.08

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/base/model.py:566: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

warnings.warn("Maximum Likelihood optimization failed to "

start_date = '2020-06-12'

end_date = '2022-10-04'

FB_values['forecast_ArMA'] = results.predict(start=start_date, end=end_date)

plt.rcParams["figure.figsize"] = (15,10)

sns.set(font_scale=2)

FB_values[['Close','forecast_Ar','forecast_ArMA']].plot(lw=2)

<AxesSubplot:xlabel='Date'>