![]()

MA, AR, and Arma

introml.analyticsdojo.com

61. Out of Sample Prediction#

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from matplotlib.pylab import rcParams

rcParams['figure.figsize'] = 15, 5

import seaborn as sns

#!pip -q install yfinance

import yfinance as yf

sns.set(font_scale=2)

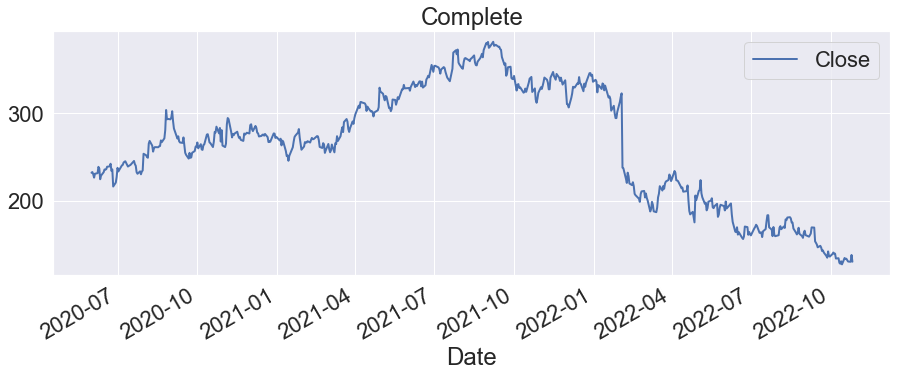

FB = yf.Ticker("META")

FB_values = FB.history(start="2020-06-01")

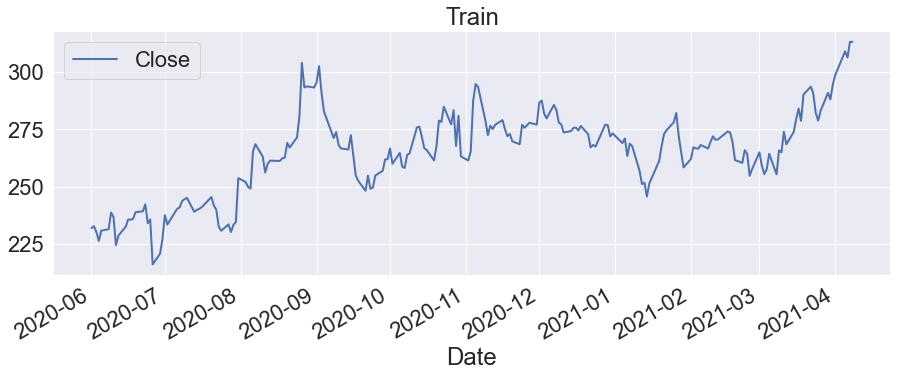

train_values=FB_values[:len(FB_values)-1000]

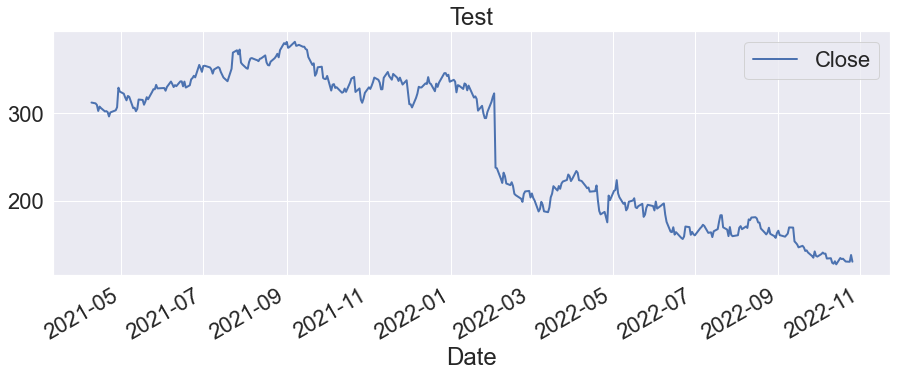

test_values=FB_values[len(FB_values)-1000:]

FB_values[['Close']].plot(lw=2,title='Complete')

train_values[['Close']].plot(lw=2,title='Train')

test_values[['Close']].plot(lw=2,title='Test')

<AxesSubplot:title={'center':'Test'}, xlabel='Date'>

from statsmodels.tsa.arima.model import ARIMA

ARMA_model = ARIMA(endog=train_values['Close'], order=(10, 0, 10))

results = ARMA_model.fit()

print(results.summary())

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/base/tsa_model.py:581: ValueWarning: A date index has been provided, but it has no associated frequency information and so will be ignored when e.g. forecasting.

warnings.warn('A date index has been provided, but it has no'

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/tsa/statespace/sarimax.py:978: UserWarning: Non-invertible starting MA parameters found. Using zeros as starting parameters.

warn('Non-invertible starting MA parameters found.'

SARIMAX Results

==============================================================================

Dep. Variable: Close No. Observations: 216

Model: ARIMA(10, 0, 10) Log Likelihood -681.035

Date: Wed, 26 Oct 2022 AIC 1406.071

Time: 20:01:06 BIC 1480.327

Sample: 0 HQIC 1436.071

- 216

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 264.4526 28.232 9.367 0.000 209.118 319.787

ar.L1 0.5871 1.666 0.352 0.724 -2.678 3.852

ar.L2 0.8793 0.858 1.024 0.306 -0.803 2.562

ar.L3 -1.2841 1.268 -1.013 0.311 -3.769 1.201

ar.L4 0.4175 2.047 0.204 0.838 -3.595 4.430

ar.L5 0.9243 0.893 1.035 0.301 -0.827 2.675

ar.L6 -1.2504 1.344 -0.930 0.352 -3.885 1.384

ar.L7 0.2804 1.940 0.145 0.885 -3.522 4.082

ar.L8 0.8848 0.699 1.265 0.206 -0.486 2.255

ar.L9 -0.2810 1.278 -0.220 0.826 -2.785 2.223

ar.L10 -0.1738 0.550 -0.316 0.752 -1.251 0.904

ma.L1 0.5007 1.674 0.299 0.765 -2.781 3.783

ma.L2 -0.4955 1.219 -0.407 0.684 -2.884 1.893

ma.L3 0.5515 0.585 0.943 0.346 -0.595 1.698

ma.L4 0.5197 1.248 0.417 0.677 -1.926 2.965

ma.L5 -0.6316 1.142 -0.553 0.580 -2.871 1.607

ma.L6 0.3860 0.726 0.531 0.595 -1.038 1.810

ma.L7 0.5651 0.855 0.661 0.509 -1.111 2.241

ma.L8 -0.4679 1.079 -0.434 0.665 -2.583 1.647

ma.L9 -0.3629 0.618 -0.587 0.557 -1.575 0.849

ma.L10 0.0409 0.399 0.102 0.918 -0.742 0.824

sigma2 30.4260 3.419 8.898 0.000 23.724 37.128

===================================================================================

Ljung-Box (L1) (Q): 0.18 Jarque-Bera (JB): 5.18

Prob(Q): 0.67 Prob(JB): 0.07

Heteroskedasticity (H): 0.85 Skew: -0.09

Prob(H) (two-sided): 0.49 Kurtosis: 3.74

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

/opt/anaconda3/lib/python3.8/site-packages/statsmodels/base/model.py:566: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

warnings.warn("Maximum Likelihood optimization failed to "

# evaluate an ARIMA model using a walk-forward validation

from pandas import read_csv

from pandas import datetime

from matplotlib import pyplot

from statsmodels.tsa.arima.model import ARIMA

from sklearn.metrics import mean_squared_error

from math import sqrt

# load dataset

FB_values = FB.history(start="2020-06-01")

train_values=FB_values[:len(FB_values)-1000]

test_values=FB_values[len(FB_values)-1000:]

test_values=test_values['Close']

train_values=train_values['Close']

history = [x for x in train_values]

history

# split into train and test sets

predictions = list()

# walk-forward validation

for t in range(len(test_values)):

model = ARIMA(history, order=(1,0,1))

model_fit = model.fit()

output = model_fit.forecast(steps=1)

yhat = output[0]

predictions.append(yhat)

obs = test_values[t]

history.append(obs)

#print('predicted=%f, expected=%f' % (yhat, obs))

# evaluate forecasts

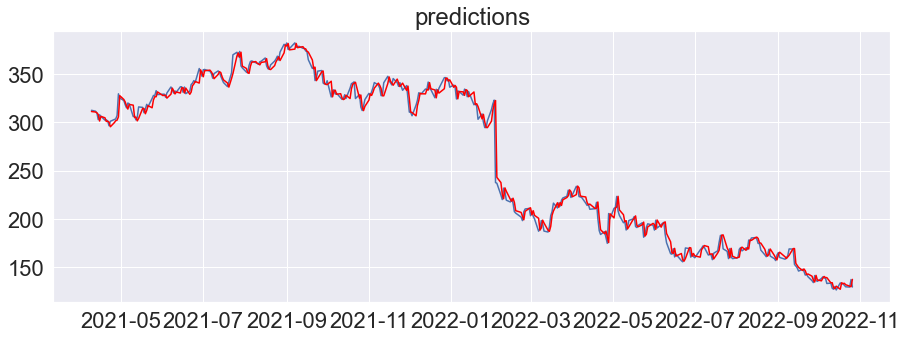

rmse = sqrt(mean_squared_error(test_values, predictions))

print('Test RMSE: %.3f' % rmse)

<ipython-input-4-f5b348368ee8>:3: FutureWarning: The pandas.datetime class is deprecated and will be removed from pandas in a future version. Import from datetime module instead.

from pandas import datetime

Test RMSE: 7.590

# plot forecasts against actual outcomes

predictions=pd.DataFrame(predictions)

test_values=pd.DataFrame(test_values)

predictions.index=test_values.index

pyplot.plot(test_values)

plt.title("predictions")

pyplot.plot(predictions, color='red')

pyplot.show()